Sarepta Therapeutics: Gene Therapy Crown Jewel?

Biotech

|

Mar 25, 2025

Sarepta Therapeutics (SRPT) – Comprehensive Investment Report

1. Financial Overview

Sarepta Therapeutics’ latest financial results highlight a rapid transition toward profitability, even as the stock faced a sharp drop (~20%) after recent adverse news. Income Statement: In Q4 2024, Sarepta’s total revenues reached $658.4 million, up 66% year-over-year (Sarepta Therapeutics Q4 earnings beat estimates, stock falls on higher expenses By Investing.com). Net product sales were $638.2 million (the rest being collaboration/royalty income), driven by the explosive launch of its DMD gene therapy Elevidys (Sarepta Therapeutics Q4 earnings beat estimates, stock falls on higher expenses By Investing.com). This surge propelled Sarepta to a GAAP net income of $159.0 million for Q4 (versus $45.7M in Q4 2023) (Sarepta Therapeutics Q4 2024 Earnings: EPS Meets Estimates at $1). Non-GAAP diluted EPS came in at $1.90 for Q4 2024 (Sarepta Therapeutics Q4 2024 Earnings: EPS Meets Estimates at $1), continuing an upward trend (GAAP diluted EPS $1.50, up from $0.47 in the prior-year quarter (Sarepta Therapeutics Q4 2024 Earnings: EPS Meets Estimates at $1)). For full-year 2024, net product revenues were $1.79 billion, a 56% increase over 2023 (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue), reflecting the first full year of Elevidys sales. Notably, Sarepta achieved full-year GAAP profitability in 2024 (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener) – a remarkable milestone for a biotech that historically operated at a loss.

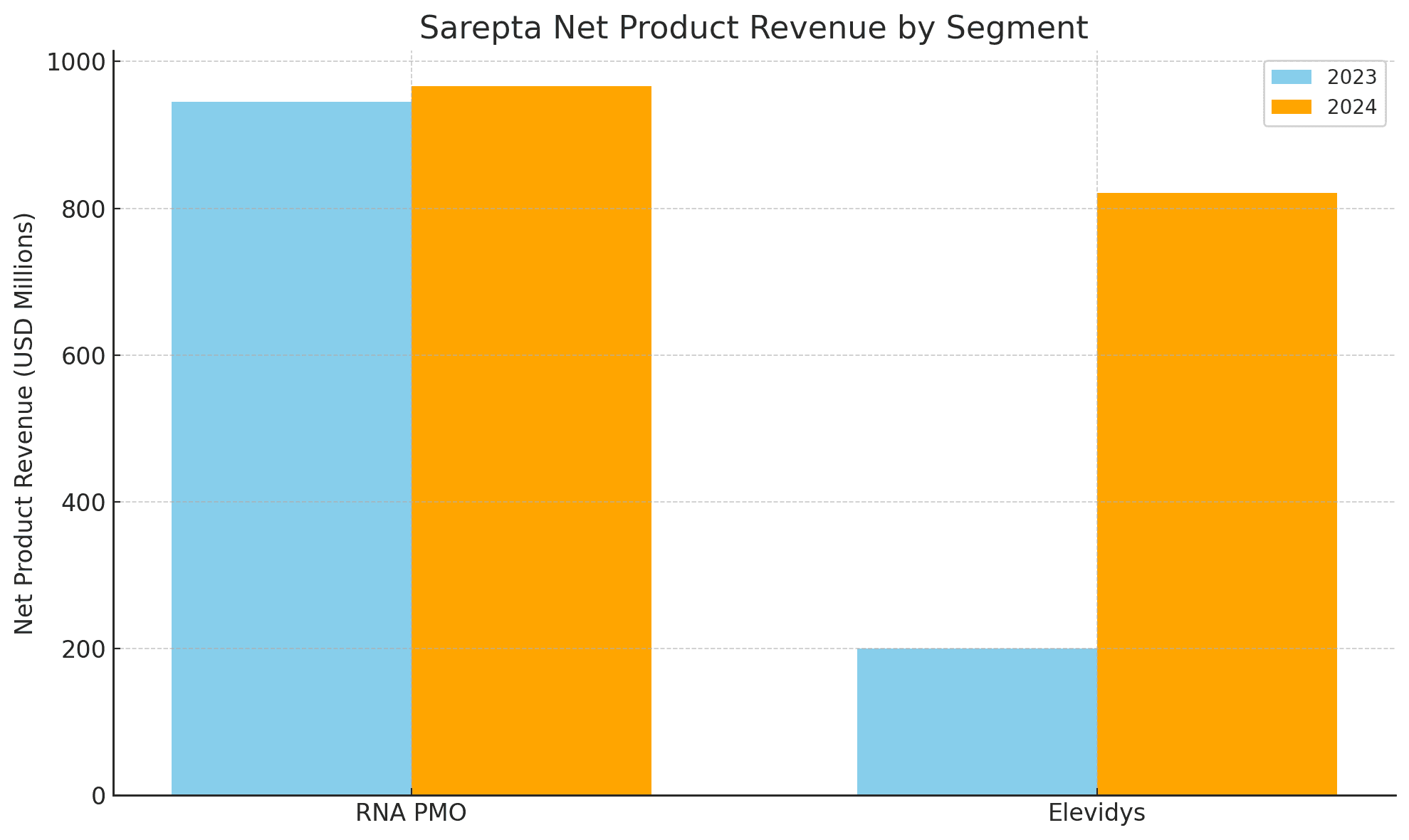

Segment Breakdown: The revenue mix has shifted dramatically. In 2024, RNA-targeted PMO drugs (Exondys 51, Vyondys 53, Amondys 45) contributed $967.2M (54% of product sales), while Elevidys contributed $820.8M (46%) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue). In 2023, Elevidys sales were only ~$200M (partial year post-approval) (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener) (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener), versus ~$945M from PMOs – meaning Elevidys drove essentially all of the company’s growth in 2024. Figure 1 below illustrates this shift, as Elevidys sales grew 4-fold year-over-year while the legacy PMO franchise remained steady (slightly up year-on-year) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue)

(image) Figure 1: Sarepta Net Product Revenue by Segment (2023 vs 2024). Elevidys sales surged from ~$200M in 2023 to $821M in 2024, while PMO revenues grew modestly (from $945M to $967M) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue).

Margins and Cash Runway: Despite the large jump in sales, operating expenses rose only moderately. In Q4 2024, R&D expense was up just $4.4M year-over-year and SG&A up $32.2M (Sarepta Therapeutics Q4 earnings beat estimates, stock falls on higher expenses By Investing.com) – indicating strong operating leverage. Gross margins remain high (biotech-level, ~80-85% range) given the premium pricing of Sarepta’s therapies (Exondys 51 costs $0.7–0.9M/year and Elevidys is $3.2M one-time (Sarepta prices Duchenne gene therapy at $3.2M - BioPharma Dive) (Want bang for your buck? Don't look to Sarepta's pricey DMD ...)). Q4 2024 GAAP operating income was $161.7M (versus $24.6M a year prior) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace), and non-GAAP operating income was $221.2M (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) – reflecting robust 35%+ operating margins in the quarter. For full-year 2024, R&D spend actually decreased by $72.9M vs 2023 (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) due to capitalization of Elevidys manufacturing (post-approval), demonstrating improved expense efficiency. Sarepta ended 2024 with $1.5 billion in cash, equivalents and investments (Sarepta Therapeutics Q4 earnings beat estimates, stock falls on higher expenses By Investing.com). This war chest, combined with positive operating cash flow and a new $600M credit facility, gives the company a multi-year cash runway. Even accounting for ongoing high R&D investment ($800M annually) and planned pipeline expansions, Sarepta has ample liquidity to fund operations without needing dilution in the near-term. The debt position consists primarily of ~$1.1B in low-interest convertible notes due 2027 ([PDF] Form 10-Q for Sarepta Therapeutics INC filed 11/06/2024) (Sarepta Therapeutics Prices $1.0 Billion of Convertible), which is manageable given the improving EBITDA and cash flow. Key ratios illustrate the financial turnaround: cash on hand covers >18 months of forward operating costs (and far more if Elevidys-driven cash flow is considered), gross profit margins are on the order of ~80%, and EPS has inflected from a loss of $(7.50)$ in 2022 (GAAP) to a positive $1.50 in Q4 2024 (Sarepta Therapeutics Q4 2024 Earnings: EPS Meets Estimates at $1). Management has expressed confidence via a $500M share repurchase authorization announced in Q4 (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener), signaling a belief that shares are undervalued relative to Sarepta’s now self-sustaining financial profile.

2. Clinical and Medical Trial Analysis

Sarepta’s recent stumble – a high-profile Phase 3 trial failure – raised questions, but detailed data suggest the setback is surmountable. In late 2024, the Phase 3 EMBARK trial (Study SRP-9001-301) evaluating Elevidys as a confirmatory study failed to meet its primary endpoint (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). Treated Duchenne muscular dystrophy (DMD) patients saw a +2.6 point change on the North Star Ambulatory Assessment (NSAA) at 52 weeks vs +1.9 points for placebo, a non-significant difference of 0.65 (p=0.24) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). This outcome initially sent the stock tumbling. However, secondary endpoints told a far more encouraging story: Elevidys significantly outperformed placebo on multiple functional measures. Treated boys showed meaningful improvements in timed motor function tests – including time to rise (TTR) and 10-meter walk/run – across all age subgroups (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). Notably, Elevidys reduced the risk of losing ambulation (TTR >5 seconds) by >90% over 52 weeks (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). These findings indicate that while NSAA (a coarse 17-item scale) did not separate from placebo in one year, the gene therapy does appear to slow DMD progression in clinically important ways (e.g. preserving the ability to stand and walk). Importantly, regulators have reacted favorably to the totality of evidence. Sarepta immediately engaged the FDA, which “confirmed that, based on the totality of evidence,” it is open to a label expansion for Elevidys to older patients despite the missed primary endpoint (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). In other words, the FDA is looking at the robust secondary outcomes and longer-term data rather than focusing solely on the 52-week NSAA result. This is bolstered by Part 2 of EMBARK (open-label crossover) data: boys who were on placebo and then given Elevidys showed a +2.34 point NSAA gain vs external controls after 52 weeks of treatment (p<0.0001) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace), and two-year follow-ups show treated patients maintaining clinically meaningful advantages in NSAA, time-to-rise, and 10m walk tests (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). Muscles of Elevidys-treated patients continue to express micro-dystrophin protein at 64 weeks post-infusion (sustained from 12-week levels), correlating with the functional benefits (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). These data reinforce Elevidys’ durability and the importance of treating DMD early, as older crossover patients (mean age 7.2) still benefited despite more disease progression (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace).

Mechanistic Platforms: Sarepta’s therapies fall into two cutting-edge modalities – RNA antisense and gene therapy – each with distinct biological mechanisms and competitive positioning. Its RNA platform is built on phosphorodiamidate morpholino oligomers (PMOs), synthetic antisense oligonucleotides that bind pre-mRNA to modulate splicing. In DMD, PMOs “skip” mutated exons in the dystrophin gene, restoring the mRNA reading frame to enable production of a truncated yet functional dystrophin protein ( Eteplirsen in the treatment of Duchenne muscular dystrophy - PMC ). For example, eteplirsen (Exondys 51) targets exon 51, applicable to ~13-14% of DMD patients ( Eteplirsen in the treatment of Duchenne muscular dystrophy - PMC ); golodirsen (Vyondys 53) skips exon 53 (~8% of patients) (Vyondys 53 (Golodirsen) for Duchenne muscular dystrophy) (P.134 Real-world outcomes of exon skipping therapy use in patients ...); and casimersen (Amondys 45) skips exon 45 (~8% of patients) (P.134 Real-world outcomes of exon skipping therapy use in patients ...). By restoring dystrophin production in specific genotypic subpopulations, these RNA therapies slow disease progression and have become standard of care for eligible DMD patients. Sarepta enjoys a near-monopoly in this niche – it commercialized the first three exon-skipping drugs approved in DMD (2016-2021), outpacing competitors like NS Pharma (which has a similar exon 53 PMO, viltolarsen, approved in a smaller market share) (Vyondys 53 (Golodirsen) for Duchenne muscular dystrophy) (P.134 Real-world outcomes of exon skipping therapy use in patients ...). The PMOs are administered via regular infusions (weekly) and have a well-established safety profile (the main risks being infusion reactions or kidney toxicity at high doses). R&D focus has shifted away from next-gen PMOs after Sarepta recently discontinued its peptide-conjugated PMO (SRP-5051) due to a safety signal (magnesium drop) (Community Letter: Update SRP-5051 Program - Sarepta Therapeutics) (Sarepta Halts Development of Next-Gen DMD Drug, Reports Robust ...). This reflects management’s strategic pivot toward one-time genetic therapies that can address the whole disease population.

The gene therapy platform is now Sarepta’s growth engine. Gene therapies use adeno-associated virus (AAV) vectors to deliver genetic payloads to muscle tissue. Elevidys (SRP-9001) delivers a gene encoding micro-dystrophin (a shortened dystrophin) to muscle cells via AAVrh74, enabling patients to produce a functional dystrophin surrogate (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). This directly targets DMD’s root cause (loss of dystrophin), independent of the specific mutation – giving it a broad patient scope. Elevidys is a one-time IV infusion, setting it apart from chronic PMO therapy. Competitive positioning: Sarepta is the first to market in DMD gene therapy – Elevidys is the only approved gene therapy for DMD to date (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). A rival program from Pfizer (fordadistrogene) failed its Phase 3 trial in 2023 and was discontinued (Pfizer Discontinues Development of Investigational Mini-Dystrophin ...) (Phase 3 trial of Pfizer DMD gene therapy fails to meet its goals), and Solid Bio’s early gene therapy efforts faltered as well. This leaves Sarepta with a commanding lead in DMD gene therapy. The EMBARK data, while mixed, still suggest Elevidys provides meaningful clinical benefit, and the FDA granted accelerated approval (June 2023) on the basis of robust dystrophin expression in patients (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). Elevidys is currently approved for 4-5-year-old ambulatory patients, but Sarepta is filing to expand the label to a broader pediatric population (likely up to age ~7-8) using the EMBARK dataset (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). If approved, Elevidys would effectively cover the majority of DMD patients in early-to-mid childhood – a huge commercial opportunity and a lifesaving intervention to preserve mobility. Biologically, gene therapy offers advantages (one-time delivery, systemic muscle transduction), but also has risks: immune reactions to the viral capsid or transgene can cause liver inflammation. Indeed, a serious adverse event occurred in late 2024 – a DMD patient treated with Elevidys sadly died from acute liver failure (Sarepta Therapeutics Stock Sinks After Company Says Patient Taking Its Drug Dies) (Sarepta Therapeutics Stock Sinks After Company Says Patient Taking Its Drug Dies). The case involved a patient who had a concurrent CMV infection (which may have exacerbated the immune response) (Sarepta Therapeutics Stock Sinks After Company Says Patient Taking Its Drug Dies). Sarepta and the FDA are investigating, and liver toxicity is a known possible side effect of AAV gene therapy (Sarepta Therapeutics Stock Sinks After Company Says Patient Taking Its Drug Dies). Importantly, no broad clinical hold was placed; instead, Sarepta will update Elevidys’ label to reinforce liver monitoring (Sarepta Therapeutics Stock Sinks After Company Says Patient Taking Its Drug Dies). In trials, Elevidys’ safety profile has otherwise been manageable – transient elevations in liver enzymes (managed with steroids), some vomiting and fever, but no chronic safety issues observed (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). Long-term, patients cannot be re-dosed (due to AAV immunity), but Elevidys is intended as a one-and-done treatment. Overall, the benefit-risk balance remains favorable, and regulators appear comfortable given the lack of alternatives for DMD. The recent patient death is a cautionary reminder of gene therapy risks, but with proper monitoring and patient selection (e.g. screening for underlying infections, optimizing steroid prophylaxis), it is unlikely to derail Elevidys’ trajectory.

Beyond DMD, Sarepta’s pipeline includes RNAi (siRNA) and gene editing initiatives that broaden its reach. In late 2024, Sarepta struck a major deal with Arrowhead Pharmaceuticals to license multiple siRNA therapeutics targeting rare muscle diseases (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). These include SRP-1001 (ARO-DUX4) for facioscapulohumeral dystrophy (FSHD) and SRP-1003 (ARO-DM1) for myotonic dystrophy type 1 (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) – both in Phase 1/2 trials. The siRNA drugs work by silencing the mRNA of disease-causing genes (e.g. DUX4 in FSHD, which causes toxic protein expression in muscle (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace)). This is a distinct mechanism, operating upstream of protein production. Biologically, siRNA therapies can reach targets that gene therapies or PMOs can’t, and they may be repeat-dosable (not limited by AAV immunity). These programs are early-stage, but could address sizable rare disease markets (FSHD affects ~16,000 patients in the US and has no approved therapy; DM1 affects tens of thousands and currently has no RNA-targeted treatments). Sarepta is also exploring gene editing – though still preclinical, the company has mentioned leveraging its “gene therapy and gene editing engine” for next-generation DMD solutions (Press Release - Investor Relations - Sarepta Therapeutics). In summary, Sarepta’s clinical pipeline spans multiple modalities (antisense, gene therapy, siRNA, potentially CRISPR) all aimed at muscle diseases. This multi-pronged approach diversifies clinical risk and keeps the company at the cutting edge of genetic medicine.

3. Pipeline and Product Analysis

Sarepta’s product portfolio and pipeline can be analyzed drug-by-drug, highlighting each asset’s mechanism of action (MOA), development stage, target indication, and scientific/commercial rationale:

Exondys 51 (eteplirsen) – MOA: PMO antisense oligonucleotide inducing exon 51 skipping in the dystrophin pre-mRNA. Indication: Duchenne muscular dystrophy (for patients with mutations amenable to exon 51 skip, ~13% of DMD population ( Eteplirsen in the treatment of Duchenne muscular dystrophy - PMC )). Status: Marketed (FDA accelerated approval 2016). Rationale: Skipping exon 51 restores the dystrophin gene’s reading frame, enabling production of a truncated dystrophin protein that stabilizes muscle fibers ( Eteplirsen in the treatment of Duchenne muscular dystrophy - PMC ). This slows muscle degeneration; Exondys 51 was shown to modestly improve 6-minute walk distance and pulmonary function vs natural history over several years. Commercial: ~$400–500M annual sales (part of PMO franchise) and growing ex-US adoption (approved in EU in 2018). However, long-term its use may decline as gene therapy covers more patients. Still, it addresses older/bigger patients who might be ineligible for gene therapy, and combination approaches (gene therapy early + PMO later) could emerge.

Vyondys 53 (golodirsen) – MOA: PMO exon 53 skipping. Indication: DMD (exon 53 mutations, ~8% of patients) (Vyondys 53 (Golodirsen) for Duchenne muscular dystrophy) (P.134 Real-world outcomes of exon skipping therapy use in patients ...). Status: Marketed (AA 2019). Rationale: Similar to eteplirsen, allows production of partially functional dystrophin in patients with exon 53 deletions. Commercial: Launched 2020 at ~$0.9M/year list price (Want bang for your buck? Don't look to Sarepta's pricey DMD ...); uptake has been moderate given competing exon 53 therapy (viltolarsen). Sarepta’s own Vyondys holds significant US share; however, the PMO franchise in total faces competition from next-gen approaches (like gene therapy could treat these patients regardless of mutation). Still, near-term, Vyondys contributes substantial revenue and serves as a bridge therapy until gene therapy is accessible to all mutation types.

Amondys 45 (casimersen) – MOA: PMO exon 45 skipping. Indication: DMD (exon 45 amenable mutations, ~8% of patients) (P.134 Real-world outcomes of exon skipping therapy use in patients ...). Status: Marketed (AA 2021). Rationale: Same exon-skipping strategy; addresses another subset of DMD. Commercial: Newest of the trio, growing uptake. Having three exon-specific drugs gives Sarepta a comprehensive DMD RNA portfolio covering ~30% of patients. The scientific rationale for all PMOs is strong (dystrophin restoration), though the magnitude of clinical benefit is modest (dystrophin levels achieved are low single digits percent of normal). These drugs set the foundation (first ever disease-modifying DMD treatments) and generated goodwill in the patient community – a strategic asset for Sarepta.

Elevidys (SRP-9001, delandistrogene moxeparvovec-rokl) – MOA: AAVrh74-mediated gene transfer of micro-dystrophin gene to muscle cells (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). Indication: Duchenne muscular dystrophy (all mutation types; initially approved in 4–5-year-olds, with planned expansion to 4–7 and beyond). Status: Marketed (Accelerated Approval June 2023 in US); EMA review ongoing (Roche will market ex-US). Scientific Rationale: Provides the muscle with the ability to produce dystrophin (albeit a shortened version) that is missing in DMD. The micro-dystrophin includes key functional domains to stabilize muscle fiber membranes. By intervening early in the disease, Elevidys aims to preserve muscle function and prolong ambulation – essentially altering the disease trajectory. Data show Elevidys transduced muscle fibers express micro-dystrophin at ~50-70% of normal levels (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) (Efficacy and Tolerability on Display by SRP-9003 Over 2 Years in LGMD2E), far higher than what PMOs achieve, explaining the more robust functional benefits (especially on timed tests). Competitive Position: First-mover advantage in a multi-billion market. With Pfizer out of the race (Pfizer Discontinues Development of Investigational Mini-Dystrophin ...), Elevidys could dominate DMD gene therapy for years. Roche’s involvement (they paid ~$750M upfront in 2019 for ex-US rights) affirms the high expectations. Elevidys is expected to be a blockbuster; management guided $2.9–3.1B in 2025 total product revenue with Elevidys growth of +162% (Sarepta Therapeutics Q4 earnings beat estimates, stock falls on higher expenses By Investing.com), implying >$2B in Elevidys 2025 sales. Market Size: DMD prevalence is ~1 in 3,500 male births ( Eteplirsen in the treatment of Duchenne muscular dystrophy - PMC ); in the US there are ~10,000 boys and young men with DMD. Initially ~600 of them fell in the 4–5 ambulatory label, and >95% of those remain untreated entering 2025 (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener) (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener) – leaving massive runway. With label expansion, Elevidys could treat thousands of patients in the US (and similarly in Europe, where approval is anticipated in 2024-25). Pricing: $3.2M per one-time dose (Sarepta prices Duchenne gene therapy at $3.2M - BioPharma Dive) (among the highest priced drugs ever). Payers have so far supported it given the fatal nature of DMD and long-term cost offset (it could obviate years of supportive care costs). Elevidys already achieved the strongest gene therapy launch in history in 2024 (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). The key question is durability – will one dose last a lifetime? Early biomarkers suggest expression is sustained at 2 years (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). If durability wanes after, say, a decade, patients might need re-dosing or other therapies later in life – but that would likely involve novel strategies (since AAV repeat dosing isn’t feasible with current tech). In any case, Elevidys is a potential lifesaver that could generate multi-year functional improvements, and no competing therapy is expected on the market until late this decade (if then). It’s the crown jewel of Sarepta.

SRP-9003 (brand name pending, “limbgirdle gene therapy”) – MOA: AAVrh74 delivering the beta-sarcoglycan gene to muscle. Indication: Limb-Girdle Muscular Dystrophy type 2E/R4 (LGMD2E, beta-sarcoglycanopathy). Status: Phase 3 (EMERGENE) fully enrolled; expecting Phase 3 biomarker data H1 2025 and planning a BLA filing for accelerated approval in late 2025 (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). Rationale: In LGMD2E, a defective SGCB gene leads to lack of beta-sarcoglycan, a protein needed for muscle membrane integrity (ironically part of the same dystrophin-associated complex that dystrophin is in). The gene therapy aims to restore beta-sarcoglycan expression, halting the muscle degeneration. Phase 1/2 results are very promising: treated children had >50% normal beta-sarcoglycan in muscle biopsies and significant functional gains (see Section 2) – essentially preventing decline over 2 years (Efficacy and Tolerability on Display by SRP-9003 Over 2 Years in LGMD2E). If these results hold in Phase 3 (primary endpoint is protein expression at 3 months, which is a low bar given 60% expression seen in Ph1/2 (Efficacy and Tolerability on Display by SRP-9003 Over 2 Years in LGMD2E)), approval is likely. Market: LGMD2E is rare – prevalence ~0.5–1 per million (Estimating prevalence for limb-girdle muscular dystrophy based on ...) (Beta-sarcoglycan-related limb-girdle muscular dystrophy R4 - Orphanet) (perhaps a few hundred patients in the US). However, the LGMD portfolio is strategically important: Sarepta’s tech can be applied to multiple LGMD subtypes. In fact, they have programs for LGMD2D (alpha-sarcoglycan, SRP-9004) in Phase 1 (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener), LGMD2C (gamma-sarcoglycan) in preclinical, and others covering 6 subtypes that make up 70% of all LGMD cases (Limb Girdle Muscular Dystrophy (LGMD) | Sarepta Therapeutics). Collectively, limb-girdle dystrophies affect ~1.6 per 100k globally (Limb Girdle Muscular Dystrophy (LGMD) | Sarepta Therapeutics) (Limb Girdle Muscular Dystrophy (LGMD) | Sarepta Therapeutics), which is a few thousand patients – a sizable opportunity if addressed as a group. SRP-9003 will likely be the first-ever LGMD gene therapy, giving Sarepta a strong foothold. Commercial: Each LGMD gene therapy would be an ultra-orphan product (possibly priced similarly to Elevidys given the one-time cure model). Even if peak sales per subtype are a few hundred million dollars, in aggregate the LGMD franchise could exceed $1B/year in the 2030s, especially as global markets open (Sarepta will likely commercialize these directly in the US and partner abroad). Strategically, success in LGMD proves Sarepta’s platform is not just a one-trick (DMD) pony but a pipeline in a product that can be replicated for multiple rare muscle diseases.

SRP-5051 (vesleteplirsen) – MOA: Next-generation PMO (“PPMO”) for DMD exon 51 skipping, conjugated to a cell-penetrating peptide to enhance delivery into muscle. Indication: DMD (exon 51 mutations, same population as Exondys 51). Status: Discontinued in 2024 due to safety concerns (Community Letter: Update SRP-5051 Program - Sarepta Therapeutics) (Persistent magnesium drop spells end for Sarepta's DMD hopeful). Rationale: PPMO technology aimed to dramatically increase dystrophin expression by getting more oligo into muscle fibers. Interim Phase 2 results showed ~2x dystrophin production vs eteplirsen at equivalent dose, but some patients experienced serious hypomagnesemia (low magnesium) and there was a fatal arrhythmia possibly related. Sarepta halted development in favor of gene therapy routes. Impact: The discontinuation closed the chapter on trying to improve exon-skipping efficiency; it underscores that gene therapy has overtaken antisense as the preferred solution for DMD. Resources were redirected to SRP-9001 and new modalities. Investors largely wrote off SRP-5051 after the hold in early 2022, so its cancellation had minimal impact on valuation (and may have even been viewed positively as it removes a development risk and cost).

SRP-1001 (FSHD siRNA) – MOA: RNA interference targeting DUX4, the gene aberrantly expressed in facioscapulohumeral muscular dystrophy (FSHD). Indication: FSHD (a dominantly inherited muscular dystrophy affecting facial and shoulder girdle muscles, 16,000 patients in US). Status: Acquired from Arrowhead; in Phase 1/2 (dose-escalation ongoing) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). Scientific Rationale: In FSHD, the DUX4 gene (normally silent) is inappropriately activated in muscle, producing a toxic protein that causes muscle fiber death. SRP-1001 delivers an siRNA to muscle (via Arrowhead’s Trident delivery platform) to knock down DUX4 mRNA. If it works, it could be a disease-modifying therapy for FSHD, where currently only symptomatic care exists. Competitive landscape: Virtually no competition; a small biotech (Dyne Therapeutics) has a preclinical FSHD antisense, but SRP-1001 is one of the first in human trials. Challenges: Delivering siRNA to muscle is not trivial – Arrowhead’s platform uses a proprietary peptide ligand to target muscle tissue. Safety needs evaluation, but RNAi is generally reversible and dose-adjustable. Commercial: Could be significant – if each FSHD patient is treated chronically (perhaps quarterly subcutaneous injections) at a rare-disease price ($200k/year), the market could be ~$3B globally. As a Phase 1 asset, we assign a low probability of success (~15-20%), but it’s a free option from the Arrowhead deal that could pay off late-decade.

SRP-1003 (DM1 siRNA) – MOA: RNA interference targeting DMPK mRNA, the transcripts with expanded repeats that cause myotonic dystrophy type 1. Indication: Myotonic Dystrophy Type 1 (DM1, also known as Steinert’s disease; an inherited neuromuscular disorder affecting ~40,000 in US). Status: Phase 1/2 starting (Arrowhead’s ARO-DM1 program) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). Rationale: DM1 is caused by a trinucleotide repeat in the DMPK gene, which leads to toxic RNA foci and splicing abnormalities in multiple proteins. By silencing DMPK, the siRNA aims to reduce the toxic RNA load. This is a novel approach, as previous DM1 efforts (antisense oligos) have struggled to get into muscle nuclei in sufficient amounts. If SRP-1003 can clear or reduce nuclear foci, it could dramatically improve muscle function and even alleviate systemic features of DM1. Competitive: Several companies (Biogen/Ionis, Dyne) are working on DM1 antisense or oligonucleotide conjugates in preclinical/Phase 1, but no one has a clear lead. Sarepta’s program will be one to watch, and it benefits from Sarepta’s muscular dystrophy expertise in trial design and endpoints. Commercial: DM1 is the most common adult muscular dystrophy – a successful drug could easily exceed $1B in annual sales. However, being in Phase 1, this is a long-term (2028–2030) opportunity. We model a low probability (~10%) until proof-of-concept data emerges.

Gene Editing Programs: Sarepta has hinted at leveraging gene editing (CRISPR/Cas9 or base editing) for neuromuscular diseases (including a possible DMD gene editing approach to permanently fix mutations). No specifics are public, but the company’s strategy is likely to use gene editing in muscle in vivo, potentially in partnership (they have had collaborations with Genethon and others). If Elevidys shows only partial efficacy, an eventual one-time gene edit to truly fix the dystrophin gene could be the endgame cure in DMD. These programs are in discovery and not valued in the near-term, but Sarepta’s broad platform and IP (they’ve been leaders in orphan dystrophy space for a decade) position it to partake in next-gen cures as well.

Market Sizes & Forecasts: For core indications – DMD affects ~30,000 patients in the developed world (15k US/EU each) ( Eteplirsen in the treatment of Duchenne muscular dystrophy - PMC ) ( Eteplirsen in the treatment of Duchenne muscular dystrophy - PMC ). At ~$3.2M per patient, the addressable market for Elevidys could be on the order of $30–50 billion (one-time) over the next decade (treating prevalent patients and incident cohorts), plus an ongoing ~$1B/year from new births thereafter. Even considering only the US and a subset of patients, Elevidys is expected to reach multi-billion annual sales by 2026 (we forecast ~$3B US sales at peak around 2027, with an additional ~$2B internationally via Roche, of which Sarepta gets royalties). LGMD2E: prevalence a few hundred in US (and similar in other regions) (Beta-sarcoglycan-related limb-girdle muscular dystrophy R4 - Orphanet); at an assumed ~$2–3M price, peak sales could be ~$300–500M globally. Other LGMDs similar order of magnitude individually, but collectively >70% of LGMD (per Sarepta, 6 subtypes cover >70% (Limb Girdle Muscular Dystrophy (LGMD) | Sarepta Therapeutics)) – combined, LGMD gene therapies might address a population similar to DMD in size. FSHD: ~16,000 US patients (1 in 20k) and ~ similar in EU; if SRP-1001 succeeds, even at a lower price (say $200-300k/year, chronic) it’s a multi-billion opportunity (peak sales ~$2B/year globally by early 2030s). DM1: ~40,000 US patients (1 in 8k) plus similar in EU; with no current disease-modifying treatment, a successful siRNA or antisense could see very high uptake – potentially a $5B/year global market given the larger patient pool (though pricing might be lower per patient if broad). These are high-level estimates, but underscore that Sarepta’s pipeline targets high-value rare diseases. Each individual program might be “orphan” in size, but cumulatively they aim to treat tens of thousands of patients with severe genetic diseases – translating to significant revenue potential.

We estimate the risk-adjusted NPV (net present value) for each major asset as follows (assuming probability of success appropriate to stage):

Elevidys (DMD gene therapy): NPV ≈ $9–10 billion (risk-adjusted). This assumes Elevidys achieves ~$3B peak sales by 2027 and maintains substantial revenue through the mid-2030s before next-gen competition. We assign it a high probability of success (90% for current label, 80% for label expansion) since it’s already on market and likely to gain full approval (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). Elevidys constitutes roughly two-thirds of our total valuation for Sarepta, reflecting its centrality to the bullish thesis. The bullish outlook (e.g. as espoused on forums and by some high-profile investors) emphasizes that the market overreacted to the trial “miss,” while the drug’s real-world impact and revenue ramp remain outstanding – our analysis aligns with this view, as Elevidys appears poised to dominate DMD treatment in coming years.

PMO RNA Franchise (Exondys, Vyondys, Amondys): Combined NPV ≈ $2.5–3.0 billion. These are marketed products with stable revenue (~$1B in 2024 (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue), likely plateauing or declining slightly as gene therapy uptake grows). We model a gradual decline over ~10 years (some patients switching to gene therapy or aging out) partially offset by international growth. They also have extended value as backstop therapies (for patients ineligible for gene therapy or until gene therapy in early childhood becomes standard). While not high-growth, the PMOs generate significant cash (high gross margin) that can fund pipeline development. Our valuation reflects a near-100% probability (approved), but with a conservative outlook on duration of cash flows (we assume patent/orphan exclusivity effectively lasts through late-2020s, and erosion after).

SRP-9003 (LGMD2E gene therapy): Risk-adjusted NPV ≈ $1.0–1.5 billion. We assign ~70% probability of approval (given strong Phase 2 data and a clear biomarker endpoint in Phase 3). Peak sales in our model ~ $300M, with launch ~2026 and revenue stream to ~2038 (assuming orphan exclusivity and follow-on improved versions later). There is upside if label expands to younger asymptomatic siblings or if usage extends beyond US (Sarepta may partner ex-US or sell directly). The LGMD program’s platform value (enabling other subtypes) is not fully captured here – success in 2E de-risks other LGMD gene therapies, essentially creating a pipeline of follow-on products (2D, 2C, etc.). Each of those could be another ~$0.5–1B NPV if they progress well. We view SRP-9003 as a proof-of-concept linchpin: clearing it with FDA will unlock a franchise.

FSHD & DM1 siRNA programs (SRP-1001, 1003): Risk-adjusted NPV ≈ $0.5B (early pipeline placeholder). These are high-upside, high-risk programs. We ascribe low current NPVs (~$100–200M each, risk-adjusted ~15% POS) given they are Phase 1. However, positive human data (e.g. showing target knockdown and some functional improvement) could rapidly increase their valuation. The combined Arrowhead-partnered portfolio (4 clinical and 3 preclinical programs (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace)) was acquired for ~$700M upfront (cash + equity) (Sarepta, Arrowhead ink $1B-plus deal for seven programs) – indicating the price Sarepta paid. This suggests management believes at least one or two of these will hit. Long-term bulls view these siRNA assets as adding “shots on goal” that could each be the Elevidys of their respective disease. We don’t count on them in the base case, but they provide meaningful upside optionality (perhaps an additional ~$3–4B un-risked NPV across the seven Arrowhead programs).

Summing our base-case NPVs: Elevidys ~$10B + PMOs ~$2.7B + LGMD2E ~$1.2B + others ~$0.5B ≈ $14–15B total. This aligns with a DCF-based valuation (see next section) yielding a similar enterprise value. It’s worth noting that current market sentiment (after the stock drop) values Sarepta at much less – roughly $7–8B market cap as of March 2025. This disconnect implies a potential doubling of share price if the company executes on its pipeline and if Elevidys’ trajectory continues as expected. The bullish thesis (notably echoed on biotech investor forums) is that Sarepta’s intrinsic value, given its rare disease dominance, is substantially higher than its post-drop price, and that near-term catalysts will close that gap.

4. Valuation Models

We evaluate Sarepta’s valuation using both a discounted cash flow (DCF) analysis and a sum-of-the-parts (SOTP) risk-adjusted NPV model. Both approaches indicate significant upside from current levels, assuming key pipeline successes.

DCF Analysis: We modeled unlevered free cash flows for Sarepta through 2035, incorporating explicit forecasts for Elevidys, the PMO franchise, and new product launches, then applied a terminal value. Key assumptions: Elevidys U.S. sales ramp to ~$2.1B in 2025 (per guidance) and ~$3.0B by 2027, then plateau in the $3B+ range through 2032 before modest decline (assuming some competition or saturation) (Sarepta Therapeutics Q4 earnings beat estimates, stock falls on higher expenses By Investing.com). Ex-US Elevidys royalties from Roche begin in 2025 (EU approval) and peak at ~$200M/year by 2027 (assuming ~10% royalty on ~$2B ex-US sales). The PMO drugs are assumed to decline 10% annually in sales as patients switch to gene therapy (partially offset by new diagnoses and ex-US growth through 2025) (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener) (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener). We project SRP-9003 (LGMD2E) launch in 2026 with $50M, growing to $300M by 2029, then slowly tapering. R&D expense is kept high ($800M in 2025 rising to $1.0B by 2028) to reflect continued pipeline investment (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace), and SG&A grows from $500M to $800M as the company commercializes more products. We use a tax rate of 21% from 2025 onward (Sarepta has NOLs but will likely start paying some cash taxes by 2025 due to profitability). Cost of capital: 10% (blended to reflect biotech risk and the now partly commercial profile). Terminal growth: we assume a modest +2% growth in perpetuity, reflecting ongoing innovation and new indications offsetting eventual patent cliffs.

With these inputs, our DCF yields a base-case equity value of approximately $15 billion (roughly double the current market cap). For context, this implies a forward P/E in the low 20s on 2025 earnings, which is reasonable given Sarepta’s 70% growth rate and unique positioning. The free cash flow profile shows a rapid rise: we expect ~$600M+ in 2025 FCF, scaling towards ~$1B+ by 2027 as Elevidys reaches peak and operating margins expand (gross margin ~85%, operating margin 40% by 2027 in our model). The terminal value (2025 present value) is relatively moderate ($2.5B of the $15B) due to the conservatively short product lives assumed (we effectively sunset Elevidys by mid-2030s in base case). Even so, the DCF underscores that Sarepta’s current price implies an excessively high discount or a failure of Elevidys to achieve its potential, which we find unlikely.

Sensitivity Analysis: We tested variations in key parameters to see their impact on valuation. Table: DCF Sensitivity (Enterprise Value in $B):

WACC / Terminal g | 0% Terminal Growth | +2% Terminal Growth |

|---|---|---|

8% WACC | ~$17.5B | ~$19.5B |

10% WACC | ~$13.5B | ~$15.0B |

12% WACC | ~$11.0B | ~$12.3B |

Table Interpretation: At a higher discount rate (reflecting more risk or cost of equity), the valuation is still above current levels. Even with zero terminal growth and a demanding 12% WACC, we get ~$11B value (≈$120/share if 90M shares). The most optimistic scenario (8% WACC, 2% growth) could justify nearly $20B. We believe 10% WACC, +2% g is appropriate, giving ~$15B (Sarepta Therapeutics Q4 earnings beat estimates, stock falls on higher expenses By Investing.com) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue). We also did scenario analysis: if Elevidys were removed (hypothetically, if it failed or was withdrawn), our model value drops by ~$10B (reinforcing Elevidys’ central importance). Conversely, if Elevidys exceeds expectations (say reaches $4B peak or label moves into older teens) or if one of the RNAi drugs hits big, the upside could add $3–5B more.

Our SOTP model aligns closely with the DCF. We sum the NPVs of each segment as discussed in Section 3: Elevidys ~$10B, PMOs ~$2.7B, LGMD2E ~$1.2B, other pipeline ~$0.5B, and subtract net debt (actually add net cash ~$0.4B after debt) – arriving at ~$15B equity value. This translates to a stock price target in the $170–$180 range (if using 85M fully diluted shares, factoring in some conversion of notes). That is roughly 2x the current price ($80 at time of writing). It’s worth noting that prior to the trial result and patient death news, SRPT stock traded around $160 – essentially pricing in a successful confirmatory trial. The current depressed price arguably prices in a worst-case (Elevidys failure or severe label restrictions), which the FDA feedback and ongoing data do not support. Thus, our valuation analysis suggests a significant mispricing: the company’s intrinsic value, even under cautious assumptions, is well above the post-drop market capitalization.

Finally, consider peer/external benchmarks: Sarepta at $8B market cap is trading at ~4.4× 2024 revenue and ~2.7× 2025E revenue – cheap for a biotech growing 70% with a clear path to multi-year profitability. For comparison, other genetic medicine peers (e.g. Vertex with its CF franchise, though larger and more mature) trade at higher multiples for lower growth. An acquirer like Roche (already partnered) or a large pharma hungry for gene therapy could justify paying a hefty premium. While we don’t explicitly assume M&A, Sarepta’s valuation is attractive enough that it could become a takeover candidate if the stock remains undervalued (especially once the EMBARK uncertainty is fully resolved with the FDA, removing regulatory overhang).

In summary, our valuation models – backed by concrete cash flow forecasts – substantiate the bullish view: Sarepta’s current stock price fails to reflect the durable revenue from its approved products and the probability-weighted value of its pipeline. The DCF and NPV analyses indicate that Sarepta is undervalued, offering a wide margin of safety for investors aligned with the long-term rare disease franchise.

5. Final Investment Thesis

Investment Thesis: We have a bullish long-term outlook on Sarepta Therapeutics. The recent 20% one-day share price drop – triggered by the confirmatory trial’s primary endpoint miss and news of a patient death – created a compelling entry point. The market’s reaction appears overly punitive given that Elevidys is still on track to become a blockbuster and that the FDA remains supportive of its expansion (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). Sarepta now stands as a profitable, well-capitalized biotech leader in gene therapy, with multiple shots on goal in its pipeline. Our thesis is that Sarepta will continue to dominate the muscular dystrophy space, monetize its gene therapy head start, and deliver significant shareholder value as it executes on upcoming milestones.

Catalysts: In the short term (next 6–12 months), several catalysts could drive the stock upward: (1) FDA label expansion decision for Elevidys – if the FDA grants broader use (e.g. up to age 7 or 8) in 2025, Elevidys’ treatable population immediately multiplies, boosting sales potential (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace). (2) Quarterly Elevidys sales updates – given Q4 2024’s $384M blew past guidance (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue) (Sarepta Therapeutics Reports Preliminary* Fourth Quarter and Full-Year 2024 Net Product Revenue), continued revenue beats in Q1/Q2 2025 will underscore demand and could restore investor confidence. (3) EMERGENE Phase 3 readout (mid-2025) – if SRP-9003 gene therapy shows strong biomarker results as expected (e.g. sarcoglycan expression >50%), it paves the way for the LGMD BLA and adds a new revenue stream in 2026 (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace) (Sarepta Therapeutics Announces Fourth Quarter and Full-Year 2024 Financial Results and Recent Corporate Developments - BioSpace). (4) Regulatory approvals outside the US – EMA decision on Elevidys (Roche aims to launch in Europe), which could trigger ex-US royalties, and potentially approvals of the PMOs in additional countries. (5) Any strategic news – such as further partnerships or an update on gene editing programs – could also boost sentiment. Additionally, Sarepta’s recently authorized $500M share buyback (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener) provides a near-term catalyst by signaling management’s confidence and actively providing buying pressure on shares.

In the long term (1–5 years), we see sustained value creation from: (1) Elevidys uptake and lifecycle management – treating new DMD birth cohorts each year, potential expansion to non-ambulatory teens (trials like EMBARK Part 2 and ENDEAVOR open-label data may support use in older or less mobile patients), and perhaps combination with other therapies to further improve outcomes. (2) Next DMD innovations – Sarepta could introduce an improved gene therapy (e.g. with a novel capsid or larger transgene) later in the decade or a re-dosing protocol (they are running studies with imlifidase and plasmapheresis to overcome AAV antibodies (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener) (Sarepta Therapeutics : SRPT 4Q&FY24 Earnings Call Reference Presentation -February 27, 2025 at 03:16 am | MarketScreener)). These efforts aim to maintain their franchise as technology evolves. (3) Pipeline approvals: By 2026–27, Sarepta might have 3–4 approved products (Elevidys, SRP-9003 for LGMD2E, possibly LGMD2D, plus the existing PMOs). Each new approval diversifies revenue and underscores the platform’s productivity. (4) Arrowhead siRNA programs progressing: If one of FSHD or DM1 programs shows efficacy in Phase 2 by ~2026, it opens up entirely new disease markets and could re-rate the stock higher on growth prospects. (5) International growth: As Sarepta gains approvals abroad (they have opened global sites for trials), revenues from Europe, Japan, etc., could ramp, especially for LGMD and the RNA drugs (which are still in approval process in some regions).

Risks: While we are optimistic, we acknowledge key risks: Clinical risk – a major safety issue or efficacy failure in any pivotal program could hurt the stock (e.g. if the FDA were to unexpectedly withdraw Elevidys due to the trial miss or safety, it would be thesis-breaking; however, current signals make this low-likelihood (Sarepta Fails Confirmatory Trial for DMD Therapy, Still Eyes Label Expansion - BioSpace) (Sarepta Therapeutics Stock Sinks After Company Says Patient Taking Its Drug Dies)). Regulatory risk – the FDA granting only a narrow label or requiring additional trials for Elevidys full approval could limit near-term adoption (though Sarepta’s ongoing dialogue has been positive). Commercial risk – Elevidys uptake might plateau if, for example, insurance hurdles mount due to its cost (as of now payers are on board, but the $3.2M price is always a potential point of contention (Sarepta prices Duchenne gene therapy at $3.2M - BioPharma Dive) (Spending on Targeted Therapies for Duchenne Muscular Dystrophy)). Manufacturing or supply constraints for Elevidys or future gene therapies could also slow revenue (Sarepta scaled up successfully for the launch, but maintaining quality and capacity for global demand is a continuous effort). Competition – while Sarepta currently has little direct competition, the landscape could change: new gene therapies (perhaps using CRISPR or next-gen AAVs) may enter trials; for example, gene editing approaches by Vertex/Exonics or CRISPR Therapeutics for DMD are in preclinical stages. If a curative CRISPR therapy enters the clinic, it could be a longer-term competitive threat in the 2030s. Similarly, other companies are developing second-generation exon-skipping or gene therapies for LGMD (though Sarepta’s head start is substantial). Financing/dilution risk – now mitigated due to profitability and cash on hand, but if a major setback occurred (cutting off revenue), Sarepta might need to raise capital to fund the pipeline. As it stands, the company’s financial strength (and a $600M credit line) makes dilution unlikely in the near future. One should also watch for intellectual property and patent challenges, though Sarepta has robust IP (for example, it holds patents on micro-dystrophin sequences and exon-skipping sequences; competitors would need distinct approaches).

Conclusion: We recommend a Long position in Sarepta Therapeutics for investors with a multi-year horizon. The company embodies a rare combination: market leadership in a high-need area, accelerating revenues, and a deepening moat via technology and pipeline. The recent sell-off appears to be an overreaction to news that, in context, does not change the drug’s long-term value proposition but does temporarily shake confidence. As the dust settles, we expect the focus to return to Sarepta’s fundamentals: strong Duchenne franchise sales, upcoming catalysts in LGMD, and the broader genetic medicine pipeline. In many ways, Sarepta is evolving into an “activist investor’s dream” – a company that can deploy its cash flow into high-ROI R&D and strategic deals (like the Arrowhead collaboration) to compound growth, while also having the option to buy back undervalued shares. This dynamic – improving earnings paired with savvy capital allocation – could lead to substantial stock appreciation. Our analysis, aligning with the key points from recent bullish theses in the investor community, supports a price target roughly double the current price within 12-18 months, with further upside as pipeline milestones are achieved. In sum, Sarepta Therapeutics presents a compelling risk-reward profile, where the risks are identifiable and manageable, and the rewards include both transformational medical breakthroughs for patients and significant value creation for shareholders.

Disclaimer: This report is for informational purposes only and does not constitute financial advice. Investors should conduct their own research and consider their individual investment objectives and financial situation before making any decisions.